Ratification Opens the Way for a New Trade Framework

On July 14, the Verkhovna Rada ratified the Free Trade Agreement between Ukraine and Türkiye with 236 votes. The document was signed in Kyiv in February 2022, while Türkiye completed its ratification process in 2024. The Ukrainian vote removes the main political obstacle to the agreement’s implementation.

However, preferential tariffs do not start automatically on the day of the parliamentary vote. The agreement is expected to enter into force two months after the final confirmation that both countries have completed their domestic procedures. Importers, exporters and logistics companies should therefore wait for the official effective date before calculating shipments under the new tariff regime.

The agreement covers much more than customs duties. It includes trade in services, rules of origin, customs cooperation, e-commerce, sanitary measures, technical barriers, intellectual property, commercial presence and trade safeguards. This makes it relevant not only to manufacturers, but also to freight forwarders, warehouse operators, customs brokers, distributors and companies planning to establish operations in Ukraine or Türkiye.

Türkiye will immediately eliminate import duties on approximately 93.4% of industrial tariff lines and 7.6% of agricultural lines from Ukraine. Additional categories will be liberalized over three to seven years. Ukraine will initially remove duties on around 56% of industrial and 11.5% of agricultural tariff lines, followed by further reductions over periods of up to ten years.

Ukrainian Commodities Meet Turkish Industrial Supply

Ukraine’s strongest opportunities are expected in products where it already has a competitive export base: agricultural commodities, processed food, vegetable oils, feed ingredients, iron and steel products, and selected industrial goods.

The agreement is particularly important for deeper agricultural processing. Preferential access for food products, oil derivatives and feed concentrates could encourage Ukrainian companies to export products with greater added value instead of relying exclusively on raw grain and oilseed shipments. At the same time, agricultural access is not unlimited: sensitive goods may remain subject to quotas, transitional schedules or protective measures.

Türkiye remains a major market for Black Sea agricultural products. The recently announced Turkish sunflower import quota for 2027 demonstrates both the scale of the opportunity and the level of competition Ukrainian suppliers will face. Tariff preferences will help only when they are combined with competitive prices, predictable volumes and reliable delivery.

Ukrainian metallurgy may also gain better access to Turkish buyers of pig iron, semi-finished products and certain rolled products. The real effect will depend on production capacity, the applicable tariff line, rules of origin and possible trade-defense measures. The agreement should therefore be viewed as an opportunity to compete, not as a guarantee of additional sales.

For Türkiye, the Ukrainian market offers a different growth model. Turkish manufacturers are well positioned in machinery, electrical appliances, vehicle components, textiles, furniture, packaging, construction materials and industrial equipment. As Ukraine gradually reduces import duties, these products may become more competitive against supplies from countries without preferential access.

The reconstruction factor significantly expands this opportunity. The World Bank estimates that Ukraine’s recovery and reconstruction needs total almost $588 billion over the next decade, with major demand expected in housing, energy, transport, industry and municipal infrastructure. Turkish contractors and manufacturers already have experience in large infrastructure projects, giving them a strong starting position in this market.

The benefits will not be distributed equally. Ukrainian light industry, furniture manufacturers and some machinery producers may face stronger competition from Turkish imports. This concern was raised during the parliamentary debate, where the government said that domestic support and investment programs would be needed alongside trade liberalization.

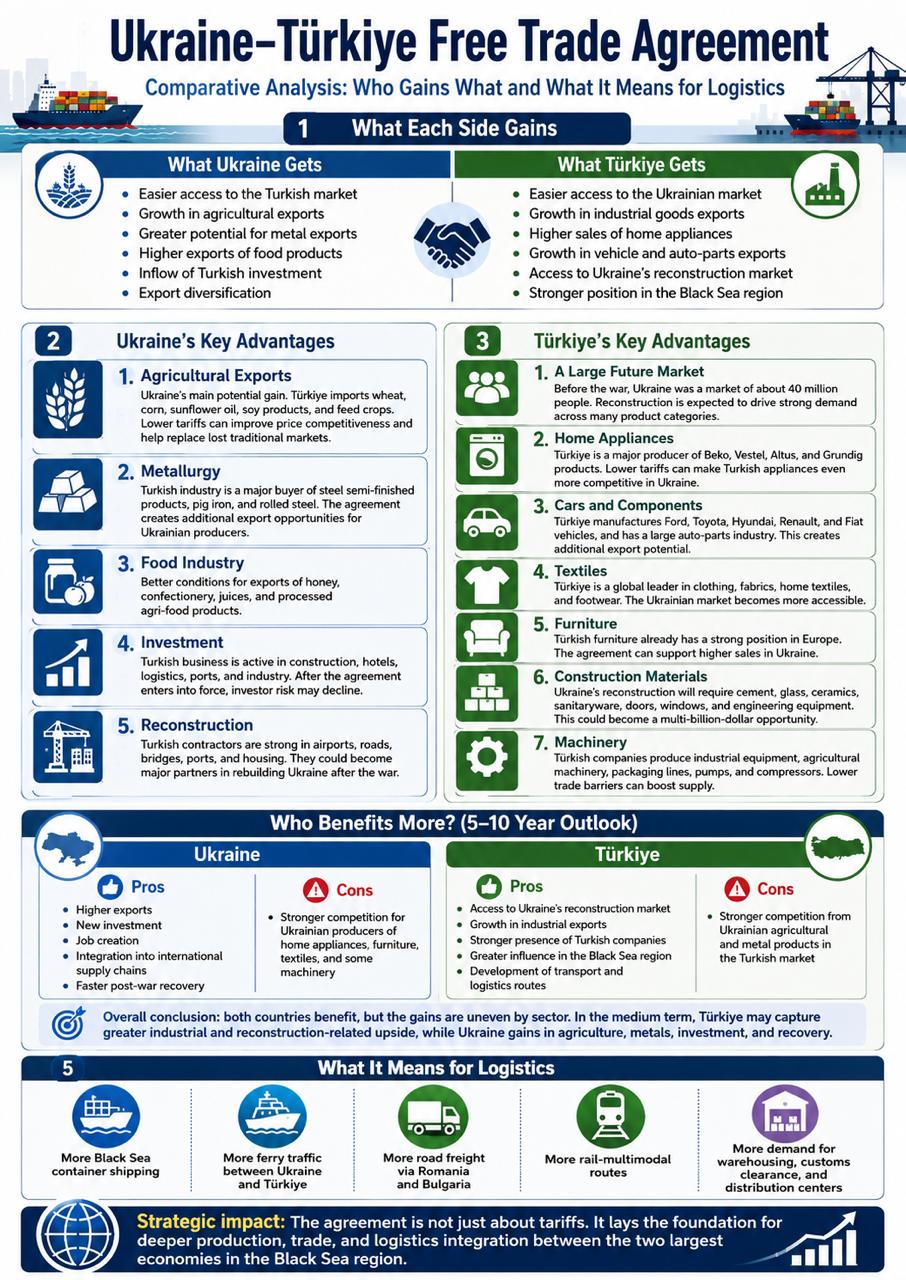

The infographic shows which Ukrainian and Turkish industries stand to benefit most from free trade and how expanding bilateral commerce could reshape transport routes, warehousing demand, and cargo flows across the Black Sea region.

Warehouses Could Become the Main Entry Point

The most important commercial effect may appear not at customs, but inside the logistics network. Lower duties can stimulate trade, but companies still need inventory, customs clearance, order processing, product labeling, returns management and delivery to the final customer.

For many Turkish manufacturers, the lowest-risk entry strategy may be to establish local inventory in Ukraine before investing in a factory or a large commercial organization. A regional warehouse allows a supplier to bring goods in consolidated batches, clear them through customs, maintain buffer stock and deliver to Ukrainian customers without waiting for a separate international shipment for every order.

This model is especially relevant for appliances, furniture, sanitaryware, tiles, machinery, spare parts and other products where delivery speed, product availability and damage control can be as important as the customs rate. A warehouse can also support product inspection, repacking, Ukrainian-language labeling, light assembly and after-sales service.

A likely distribution system would combine several types of locations. Warehouses near Ukraine’s western border could serve road and multimodal cargo arriving through Bulgaria and Romania. Facilities in the Kyiv region could support national distribution and access to the country’s largest consumer and business market. The Odesa and Danube regions could handle maritime cargo, agricultural exports, project logistics and goods connected with the Black Sea corridor.

Ukraine’s ports continue to handle substantial volumes despite the security risks. As K2Cargo News reported, Ukrainian ports processed more than 40 million tons of cargo during the first months of 2026. Their continued operation creates opportunities for direct Black Sea trade with Türkiye, although sailing schedules, insurance and infrastructure risks remain decisive.

Road transport through Türkiye, Bulgaria and Romania will remain important for higher-value, time-sensitive and smaller shipments. Rail-road combinations and the Danube ports can provide additional capacity when maritime schedules or border conditions become unpredictable. The war has already shifted more Ukrainian trade toward road transport and western crossings, increasing transit times and logistics costs.

For Ukrainian exporters, warehouse infrastructure will be equally important. Grain, processed food, honey, confectionery, metal products and industrial cargo may require consolidation, quality control, packaging, certification and temporary storage before shipment to Türkiye. Temperature-controlled facilities will be necessary for food categories with strict shelf-life requirements.

Geopolitics Pushes Investment Eastward

The free trade agreement is being introduced as global trade becomes increasingly fragmented by geopolitical conflicts, sanctions and disruptions on traditional maritime routes. In this environment, international institutions and professional investors are paying greater attention to regional production chains and transport corridors capable of connecting Europe, the Black Sea, the Caucasus, Central Asia and the Middle East.

Capital flows already indicate where part of this interest is moving. The European Bank for Reconstruction and Development invested a record €2.7 billion in Türkiye in 2025, with 91% directed to the private sector. Ukraine was simultaneously the Bank’s main investment focus in Eastern Europe and the Caucasus, where annual financing reached a record €3.7 billion. The EBRD also remains Ukraine’s largest institutional investor and is financing energy, critical infrastructure, trade and private-sector resilience.

This does not mean that international analysts see Ukraine and Türkiye as risk-free markets. Ukraine remains exposed to war-related infrastructure and logistics disruption, while Türkiye faces inflation, energy costs and regional instability. However, both countries occupy strategic positions that cannot easily be replicated: Türkiye controls access between the Black Sea and the Mediterranean and has a large industrial base, while Ukraine combines agricultural resources, metallurgy, access to European markets and one of the world’s largest future reconstruction programmes.

The parliamentary rationale for ratification follows the same logic. The Verkhovna Rada described the agreement as an instrument for long-term bilateral cooperation, market expansion and modernisation of Ukrainian production. The Ministry of Economy added that it should attract investment and integrate Ukrainian manufacturers into regional value chains. Updated Pan-Euro-Mediterranean rules of origin will allow companies to use Turkish materials and components while preserving preferential status for qualifying exports to the European Union.

For logistics companies and property investors, the strategic conclusion is clear. If trade and production links shift eastward, demand will grow not only for transport but also for physical infrastructure between the manufacturer and the buyer. Warehouses, customs facilities, consolidation centres, cross-docking terminals and regional distribution hubs in Ukraine can become the operational foundation for Turkish companies entering the market before reconstruction demand reaches its peak.

Tariff Savings Alone Will Not Win the Market

The agreement creates opportunities, but it does not remove the operational risks of trading with Ukraine. Companies must still account for wartime security, changing port conditions, border queues, insurance, currency exposure, customs inspections and fluctuating transport capacity.

Before the agreement takes effect, importers should identify the correct HS codes for their products, check the phase-out schedule and determine whether a tariff quota applies. Preferential treatment will depend on compliance with the rules of origin. Goods cannot receive benefits merely because they were dispatched from Ukraine or Türkiye; companies will need documentation proving their qualifying origin.

The final landed cost should include international transport, customs brokerage, storage, handling, domestic distribution and the cost of maintaining safety stock. For bulky goods, an inefficient warehouse or expensive last-mile operation can consume the entire benefit created by a lower import duty.

The agreement therefore creates a market not only for cargo transportation, but also for professionally managed warehousing. Customs and bonded storage, cross-docking, temperature-controlled facilities, outdoor yards, fulfillment services and regional distribution centers could become essential infrastructure for the next stage of Türkiye–Ukraine trade.

The companies most likely to benefit will be those that enter the market before cargo volumes accelerate. For Turkish suppliers, securing flexible warehouse capacity and a local logistics partner can be a faster and less capital-intensive first step than building their own infrastructure. For Ukrainian exporters, reliable consolidation and access to Black Sea logistics will determine whether preferential market access becomes actual sales.

Read also: Ukrainian Ports Handle Over 40 Million Tons of Cargo